One of the areas that has fascinated us at Lightspeed has been software for India’s small businesses. With 60M MSMEs, India is the largest base of MSMEs in the world, after China. Over 1 Trillion dollars of trade flows through these relatively unorganized channels and there is barely any software or technology that even touches these transactions and for valid reasons – traditionally, distribution to these small businesses has been operationally intensive and has required an army of agents.

Several of our portfolio companies are already building products for this sector – Oyo rooms, Magicpin, Udaan and OkCredit to name a few and we strongly believe that a lot many will follow. With all these investments, we decided to deep dive into MSMEs in India to collate learnings from our portfolio, understand the gaps that still exist in the market and build a point of view on how one can think of scaling and monetizing when building for this sector. We spoke to experts in the industry – folks who had been building for MSMEs – and also conducted a survey with over 1000 MSMEs (B2C) split across sectors and across Tier 1 and Tier 2 cities in India. Here’s what we found:

India’s MSMEs need Micro-software:

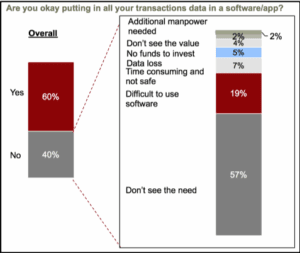

Our survey results clearly indicated that a majority of the merchants/store owners were willing to use software and save business data on an app but struggled because most of them didn’t understand the need for using software and often found software cumbersome to use. This makes absolute sense if you think about it. When it comes to these businesses, the owner is the HR head, the accountant, the salesman and the head of procurement. He is too busy to spend time adapting to complex, clunky software. Mobile is the way to go for this audience. We will see a new breed of software emerge – a category that I am calling, “micro-software”. Micro-software will essentially be a number of utilities stitched together intelligently with a specific focus on making them easy to discover and use without making the product “rich with features”.

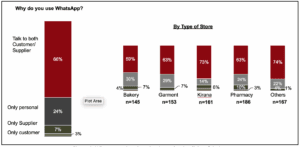

Take Whatsapp for instance – you can take and share photos, videos, audio, location and even make payments, all from a single chat screen. There are no clunky menus and no hidden features that are triggered from “settings”. Whatsapp is a very complex product with an incredibly simple interface. In fact, the one software that micro business owners personally used most is Whatsapp – to communicate with both their sellers and buyers and primarily due to its simplicity of design.

Product first thinking and top of the line customer support is key in order to scale:

A typical small business owner is generally in business with people he doesn’t fully trust. If his credit providing vendor decides to increase prices or sends him poor quality goods, then refuses to take them back, there is little he can do. Same lack of trust applies on the seller side. Surprisingly, it isn’t uncommon to hear sellers say that they don’t intend to grow their business too fast. Top reason – lack of trust in a new buyer and his ability to return credit.

Designing for trust is critical in this segment. Your customers first and foremost need to trust you as a company. With Ok Credit for instance, for the longest time, their customers couldn’t understand why the app was available to them for free! They had questions around privacy, data security, etc. Founders would get Whatsapp messages/support queries all day and the volume was so high that all members of the team would take turns answering very basic questions. Today, the team has automated most of its customer support and have just one support person who manages their massive (over 1 million merchants) registered user base. The experience for merchants is delightful and trust-inducing where most of their questions get answered instantly and for others, there is instant support available. In the case of marketplaces like Udaan, customers need to trust each other. As such, ensuring good behavior on seller and buyer side by carefully designing the behavior protocol on the app, is a key focus area for Udaan.

Both these apps enjoy enviable retention and engagement due to their product first approach to feature design and support. These teams have spent hours with their customers understanding their pain points and designed to ensure user trust – a problem that is easier to solve in theory than in practice.

Distribution is getting easier. There is a huge word of mouth potential and acquisition costs are dropping steadily

Most MSMEs are now reachable through digital advertising

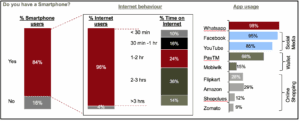

Majority of the small business owners across tier 1 and tier 2 towns use smartphones and internet for at least 1-3hrs a day and spend most of their time on Whatsapp, Facebook or Youtube, making them more accessible through digital marketing

We also believe that if features are designed the right way, it is entirely possible to scale organically and without feet on street. OkCredit, for instance, scaled almost entirely organically for the first 1.5 years (70% of their base until recently was acquired organically).

There is also strong word of mouth behavior in this segment. For instance, in most localities, there is one store owner that bears strong influence over others – take a small restaurant owner in a locality, for instance. In all likelihood, neighborhood store owners go to this restaurant for breakfast. Acquiring the restaurant owner can as such, lead to strong word of mouth with other merchants in that locality. Another similar category is chai and cigarette shop owners.

That SMBs will not use software is untrue

Day to day business management for MSMEs is cumbersome and time-consuming, to say the least. Huge gaps continue to exist

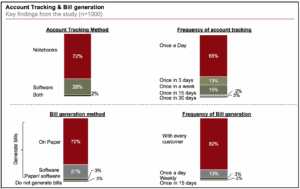

> Most manage their accounting, inventory, credits, etc. on paper/in a notebook

> Irrespective of the city or business category, 80% of the store owners spend time tallying their accounts at least once in 3 days; more than 65% tally accounts every day

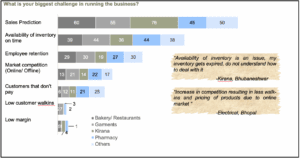

Among the biggest challenges, most businesses across sectors cite sales prediction and inventory management as their biggest pain point.

We believe that MSMEs in India will be more than willing to adopt software that helps make day to day business management easier. It will, however, require that products be designed for extreme simplicity.

Credit as an offering will not ensure monetization off the bat. One should expect speed bumps along the way

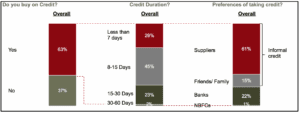

Credit is no doubt, underpenetrated. Tier 2 store owners, in general, are more credit-starved and rely heavily on credit from friends/family vs credit from suppliers. Credit from suppliers is more readily available for Tier 1 businesses. Over 70% of the store owners prefer taking credit from friends and family or suppliers, over taking loans from banks or NBFCs

However, providing credit as a service will not be as straight forward. Current account penetration among MSMEs is lower in Tier 2 cities compared to Tier 1, whereas Tier 2 is where credit demand is higher. Digital payments penetration is also lower in Tier 2 cities compared to Tier 1, adding further complexity to managing credit collections.

Opportunity to create horizontal solutions

We discovered during our survey that most MSME retailers were similar in how they ran their businesses. Lots of pen & paper, poor inventory control, heavy reliance on credit, small establishments with under 10 employees, similar education levels, similar needs and concerns. It was evident that there was tremendous potential for creating solutions that pan across verticals. Pharma, restaurants and hotels are notable exceptions, where software usage, credit availability and digital payments penetration are all higher in comparison and specific business problems/pain points differ from most other retailers.

When we look at survey results like these, we need to stand up and take notice. India’s MSMEs have come a long way. They have embraced smartphones, internet, technology and digital payments, yet the segment is software-starved. While most businesses around them have moved on, MSMEs are still stuck in the world of pen and paper, manually managing their accounts on a daily basis.

We believe that design philosophies for the MSME segment need to be similar to that for consumer products and that good software for MSMEs will see engagement and retention similar to that for the best of consumer products. The bar on product thinking is high and the rewards for cracking it are sweet! We at Lightspeed are bullish on India’s MSMEs. If you are building for them and are a believer too, write to me at harsha@lsip.com

Authors