Advancements in Large Language Models (LLMs) have emerged as a critical catalyst in the adoption of technology in the legal industry. The intersection of law and artificial intelligence has the potential to revolutionize the practice of law, making it more efficient, accessible, and cost-effective. To be sure, legaltech isn’t for the faint of heart. It’s an industry with a decades-wide graveyard of startups who have tried and failed to disrupt law with software. So why haven’t there been many legaltech winners historically and why do we believe AI-based software will be any different?

Why haven’t there been many winners in legal tech historically? And why is it any different now?

For over two centuries, the business model of a law firm has experienced little-to-no innovation due to a number of reasons that have contributed to the friction of legaltech adoption.

- Analytical vs. Generative technology: Prior to LLMs, the automation capabilities were not up to par to generate and streamline legal workflows. As a result, the technology focused on extractive use cases (i.e., data pulls which take up 20% of paralegal/attorney work) rather than generative use cases (drafting and summarization which take up 80% of the paralegal/attorney work), which provided minimal depth of automation. The value added was minimal.

Why does it work now? Depth of automation can now be achieved – AI-powered software offers a 10x improvement in the day-to-day experience of an attorney as compared to a 2x improvement from extractive techniques before. This saves them 10x time and cost, thus improving efficiency drastically. The technical innovation of LLMs can now uniquely be curated to legal workflows. - Adoption hesitancy: Attorneys are good at their jobs because they hold certain qualities, one of which is being risk-aware. As a result, selling to this persona is quite hard – since the automation technology was not there nor was it as accurate as it is now, there was always skepticism from attorneys on adopting software.

Why does it work now? Greater willingness to adopt software due to client pressure – Historically, the primary driving factor in getting attorneys to change behavior is for their end clients to put pressure on their practice. Over the past ten years, the company that demonstrated this well is Carta. Initially, Carta tried to sell to law firms with little success. They then started selling to startups, which then put pressure on startup attorneys to adopt Carta to help clients maintain cap tables and file their 83(b)s digitally, etc. We can expect client expectations on efficiency to rise with the exposure of LLMs to put similar pressure on attorneys to act more efficiently to retain their clients. For example, there is anecdotal evidence of clients pushing back on attorneys’ billing hours for “legal research” as clients expect faster turnaround times given LLM preliminary outputs. It’s the early days, but we expect this pressure to become more concrete over the next few years. - Perverse incentive from the legal business model: The common sentiment in the industry is that it is easier to sell software that makes attorneys less productive than it is to sell them software to make them more efficient due to the business model construct of ‘billable hours.’

Why does it work now? Movement towards contingency fee/flat fee model – with the potential for new technologies to make lawyers 10x more efficient, law firms are faced with the need to augment the billable hour with more value-based pricing and flat fee models, which better incentivize the efficiency that clients are beginning to demand from their attorneys. As evidenced by Wilson Sonsini’s flat rate general corporate services offering for startup legal work, which leverages a combination of software and personalized service, select Biglaw firms are transitioning certain billable hour practices to flat rate fees in order to serve client interests. We expect lower margin practices to be first movers in legal software adoption as they see the incentives around process improvement with technology (and subsequently will pass the cost to clients).

With all the factors resisting efficiency, the legal market has been slow to adopt technology: (1) lawyers have been tech laggards due to the (2) asymmetric downside for errors in legal work, (3) heavy text and unstructured data that wasn’t able to be processed accurately prior, (4) few verticalized systems tailored to law (most software were horizontal that couldn’t be properly retrofitted), and (5) a business and pricing model that doesn’t reward investments to increase efficiency.

Despite the ripe opportunity to bring technology to the legal industry, it’s only been in the last few years that we have finally started to see larger exits in the market. The key notable successes have been: SpringCM (acq by DocuSign for $220M in 2018), Exari (acq by Coupa for $215M in 2019), Casetext (acq by Thomson Reuters for $650M in 2023), LegalZoom ($2B market cap).

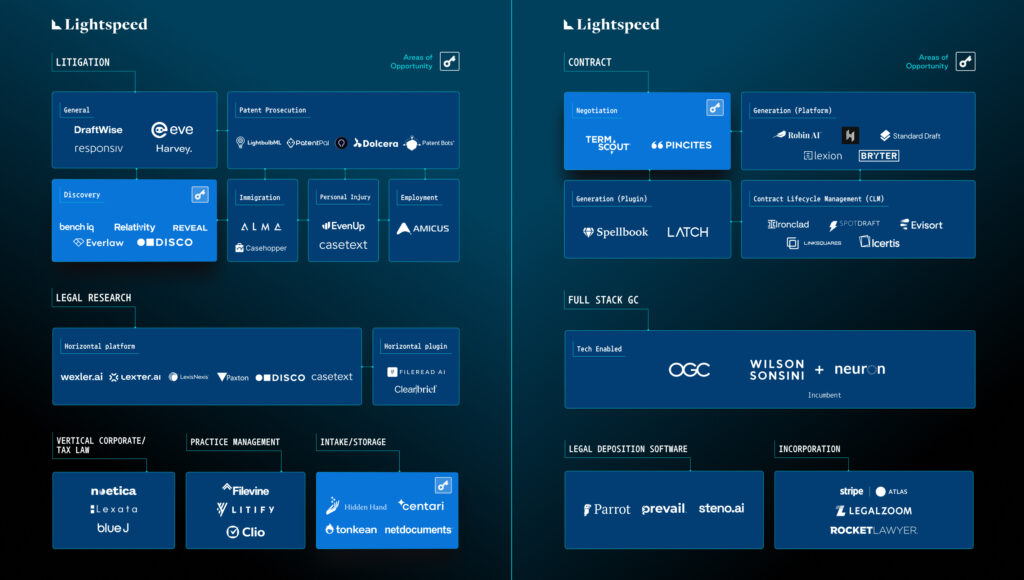

Market Map: Areas of Opportunity

Outlined below are the major categories and areas we believe are ripe for disruption

This market has a natural bifurcation of startups selling to either law firms or in-house legal counsel due to the vast difference in persona, business needs, and workflows.

There are a few areas we find most promising, mainly driven from certain factors of the business that drive incentive for software adoption. The categories are the following:

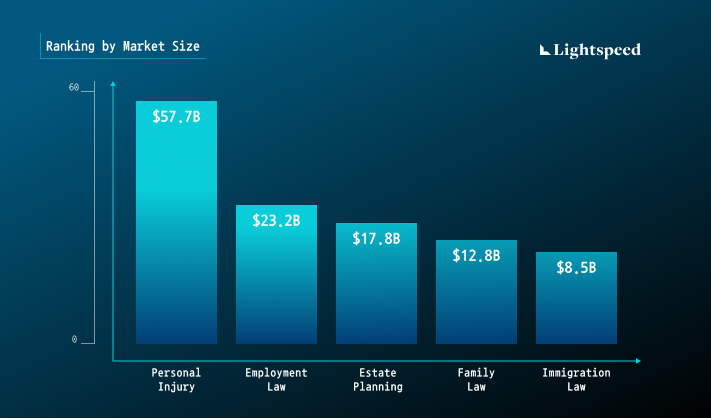

- Legal practices with contingency fee/flat fee business model, as it puts pressure on attorneys to maintain efficiency and constantly grow their practice (SMBs are strapped on resources). High volume, contingency fee driven litigation practices makes it ripe for disruption as well. Within this, repetitive form-based documents with little variation is low risk yet high ROI for GenAI x Legal use cases. This is usually associated with time sensitive deadlines, where legal use cases have deadlines to adhere to, requiring attorneys to act swiftly. This is coupled with the fact that these specific markets are highly fragmented and the majority of the market are SMB law firms – attorneys have pressure to constantly grow their practice without adding more human overhead.

- If selling towards Biglaw, it’s from a document processing standpoint or search/ediscovery. In particular, low volume, high upside litigation cases where “cracking the case” by identifying key facts incentivizes attorneys to adopt technology despite being on the billable hour.

- One example is BenchIQ which is solving deposition search. The software allows attorneys to do something they couldn’t do before. It allows them to research/access data they wouldn’t have done in order to improve the outcome of the cases. This way, they can justify passing on this cost to clients and the software is aligned to the benefit of more revenue which outweighs the perverse incentives of the billable hour.

- Areas of law with routine updates for regulatory changes

- E.G. for Immigration law – USCIS routinely updates its forms and documents, requiring quick actions from attorneys.

- Platforms that help companies stay compliant with new regulations from federal agencies (SEC, FDA, or any new AI regulations).

Specific product characteristics we are excited about

- Bringing control to attorneys: the software slots into existing workflows seamlessly/causes minimal disruption. The software is “collaborative” with the right level of permissioning for personas, functionality, and automation. This requires deep product/user understanding on workflows to deliver outcomes and services, not just GenAI software.

- Extensible enough to allow flexible formatting (something attorneys care a lot about!) but takes a structured POV on these workflows

- Better client experience: Happy clients, happy attorneys.

Areas we are less excited and common pitfalls seen from Generative AI legal tech startups

- Product scope that is too broad: Unlike the attractive “platform vision” for general SaaS companies, we believe the winners in legal tech will be companies that take a pointed approach to solving 2-3 key workflows given the highly verticalized nature even within the legal market. The common skepticism in legal tech is, “If this product is so horizontal/ broad, what does it really do?”

- Problem oriented vs Solution oriented: The job of an attorney is high stakes, so the margin for error is often zero. Selling to this persona requires building software that can be easily ingrained in their workflow or mirror that of their workflow (but automated) with a human check at the end. One cannot just sell “GenAI software” and expect it to be adopted without intimate knowledge of the workflow. Companies that succeed focus on the jobs to be done and not just how cool the LLM tech is. We are less excited about companies selling just software and not the full end to end outcome.

- Selling to in-house counsel: Legal teams are inherently cost functions and we believe the TAM is capped unless the software sold can be extended towards revenue generating functions like Sales/GTM. This is commonly the case with contract management software. Another emerging exception we see is around legal tech companies selling to enterprise GC legal teams. They have sizable Biglaw spend and we are seeing companies calculating what can be done in-house vs. what is currently outsourced to Biglaw and potentially being amenable to shifting legal spend from outside counsel to software spend to help automate route, low risk tasks (i.e. drafting).

- Building full stack services + tech in legal: The operational complexity of scaling a law firm and building a technology company gets increasingly complex as clients scale. This was felt when I was helping scale Atrium in the early days. And while the depth of automation is present thanks to the advent of LLMs, the challenges related to the operational complexity still exist with Atrium’s exact business model. The vision was broad: grow with seed startups as they scaled to Series A, B, C etc. However, the ratio of general counsel services to specialists services starts to flip as companies scale. Eventually, the high ACV legal work lies in specialist services which are incredibly hard to automate. As co-founder Augie Rakow says, “Atrium died from self-inflicted complexity”.

Musings about the future

While the adoption of AI may be booming across other industries, if legaltech’s history serves as any indication, that adoption will be more measured in the legal industry. Almost every Biglaw firm may now have a “generative AI working group,” but lawyers are still hard sells and the legal business model has still not truly shifted away from the billable hour, meaning that time-saving technologies may not actually have the ROI that legaltech founders think they do in the eyes of attorneys and law firms. Despite law firm sentiment being at an all time high, it may just be that: a flash in the pan moment. Both fantastic for startups: a ripe time to build, with vast markets to go after and incorporate AI technology/agentic solutions. But also a word of caution: it’s important to be thoughtful on how to build software for lawyers. They are unforgiving personas, so it’s critical to understand their workflows intimately to build software that deliver and compound value to them on a daily basis.

Still, the advent of LLMs and the increasing client pressure on law firms to use technology to provide legal services more efficiently is seeing some forward-thinking firms testing both the technology waters and the attendant business model changes needed to support the tech-enabled legal practice of the future. How quickly the rest of the industry follows, however, is an open question and may be directly related to how quickly alternative fee arrangements can unseat the billable hour.

Wilson Sonsini’s Chief Innovation Officer, David Wang, explains “Law firms have to learn to refocus on the customer. We will start to see the first competitively irresistible capabilities in the near-to-medium term thanks to AI. If we do not harness this power to offer higher quality, faster, and differentiated services, someone else will, and our customers will vote with their feet. It’s that simple.”

Until law firms shift to more customer-centered service models, legaltech founders will still be tasked with the challenge of selling time-saving software to firms that bill by the hour. Legaltech founders need to take this reality into account when designing for and selling to law firms, and by the same token law firms should be deliberate about proving out both the benefit of new technologies to a given practice area and how they may need to alter pricing models to reap those benefits.

Hopefully the staggering potential time savings derived from LLMs and AI-driven legaltech are what finally prompt business model changes in the legal industry, because once those changes take hold, the adoption of efficiency-driving technologies will be loosed upon a multi-billion dollar industry and we may finally see winners in not just legaltech, but among lawyers, clients, and law firms alike. The silver lining is that the belief of AI-driven law firms cannibalizing the ‘billable hours’ vestige to create something new that is work-/output-based may finally come to fruition as ChatGPT capabilities are forcing law firms to innovate to drop their fees.

Thank you Annie Datesh and David Wang of Wilson Sonsini, Augie Rakow, Lyna Kim and Mehul Arora of Lightbulb ML, and my team (Arif Janmohamed, Alex Kayyal, Antoine Moyroud, Dev Khare, Guru Chahal, Paul Smalera, Raviraj Jain) for providing feedback on drafts of this post.

Authors